.svg)

Get a Demo

Interested in trying Goodie? fill out this form and we'll be in touch with you.

Oops! Something went wrong while submitting the form.

.svg)

.svg)

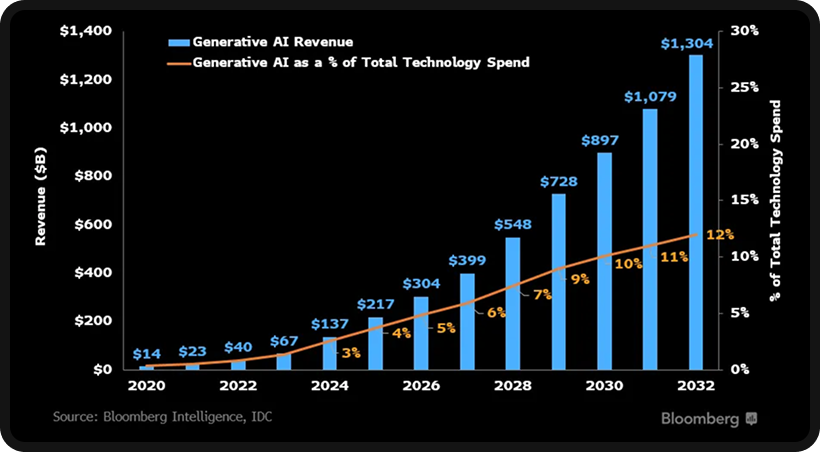

Now that the scale of capital deployment, the strategic positioning of major players, and the infrastructure requirements represent the most significant technology investment wave since the commercialization of the internet, investments in AI have reached an inflection point. What we're witnessing is a reallocation of capital that will determine which companies, industries, and nations maintain economic relevance over the next two decades.

The transformation extends far beyond Silicon Valley boardrooms and venture capital partnerships:

This investment surge represents a recognition that artificial intelligence is becoming the fundamental operating system for modern business. Companies that fail to build substantial AI capabilities risk the same fate as those that ignored the internet revolution in the 1990s or mobile computing in the 2000s.

The difference is that the AI transition is happening faster, and requires larger capital commitments than any previous technology shift.

The investment figures emerging from corporate earnings calls and government announcements reveal a seismic shift in technology capital allocation that dwarfs previous corporate spending cycles.

Major tech companies plan over $1 trillion in combined spending by 2027, according to an analysis by J.P. Morgan. This commitment represents close to 2.5x the annual revenue of Microsoft, and demonstrates the strategic priority these companies place on AI.

The urgency driving these investments has intensified in recent months:

These commitments reflect a shift in corporate risk tolerance. Traditional technology companies historically spread investments across multiple product lines and technologies to hedge against market uncertainty.

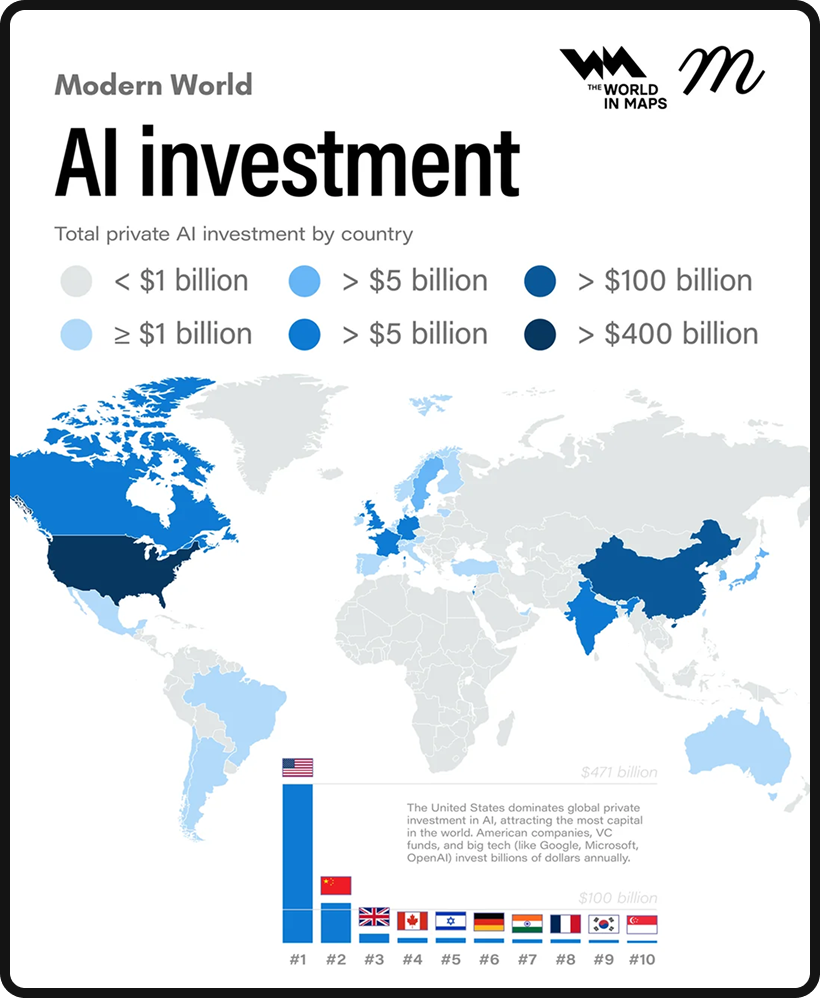

The US led private AI investment in 2024 with $109.1 billion, while China managed $9.3 billion, and the UK reached $4.5 billion. This advantage provides American companies with resources for talent acquisition, infrastructure development, and market expansion.

However, the geographic concentration creates both opportunities and vulnerabilities. While U.S. companies benefit from access to capital and talent, they also face increased regulatory scrutiny and potential backlash from international competitors.

The competitive dynamics have created what economists describe as a "Red Queen effect," where companies must invest in AI capabilities to maintain their current market position. Generative AI funding reached $33.9 billion globally, an 18.7% increase over 2023, according to Stanford's AI Index Report. More significantly, 78% of organizations worldwide reported using AI in 2024, up from 55% in 2023.

This adoption velocity has created a cycle where competitive pressure drives further investment, which accelerates capability development, which creates additional competitive pressure.

The acceleration in funding has been remarkable, but the quality and focus of investments have also evolved. Early AI investments often targeted broad research initiatives or speculative applications. Current investments focus on specific business applications with measurable returns on investment. Companies are moving from experimental AI projects to deployments that impact revenue generation and cost reduction.

The most sophisticated technology leaders recognize that AI advancement requires solving fundamental infrastructure challenges. Meta, Google, and CoreWeave announced over $90 billion in investments targeting AI and energy infrastructure, according to Reuters reporting. This strategic coupling of AI and energy investment reflects an understanding that computational capacity means nothing without a reliable, affordable, and sustainable power supply.

Building AI data centers requires computing hardware and specialized cooling systems, networking infrastructure, and proximity to renewable energy sources. The most advanced AI training runs can consume as much electricity as small cities, making energy infrastructure as critical as semiconductor capacity. Companies that solve the energy equation will gain decisive competitive advantages in AI capability development.

Google's infrastructure strategy demonstrates this integrated approach with unprecedented scale and sophistication. The company will inject $25 billion over two years into AI data centers in the PJM regional grid, which covers the mid-Atlantic United States. Critically, included in the investment is more than $3 billion to upgrade two hydropower plants that supply renewable energy to data centers.

Infrastructure investments are also driving innovation in data center design and operation. Traditional data centers were optimized for general computing workloads with predictable power consumption patterns. AI workloads create different demands, with intense computational bursts followed by periods of lower activity. New data center designs incorporate advanced cooling systems, modular power distribution, and even energy storage to handle these variable demands.

This integrated approach reflects lessons learned from earlier technology buildouts. The dot com boom of the late 1990s saw massive investments in fiber optic networks and data centers, but many projects failed because they didn't account for the full infrastructure stack. Google's current strategy addresses compute capacity and power generation, transmission, cooling, and environmental sustainability in a coordinated framework.

The energy investment extends across the competitive landscape with similar integrated approaches:

These investments signal that AI leadership requires controlling the process from software algorithms to physical infrastructure to energy generation.

The most successful AI investment strategies align with government priorities and policy frameworks in ways that create reinforcing benefits for both public and private sector objectives. The US federal government, along with private sector partners, announced a $90 billion investment targeting AI and energy infrastructure growth, according to New York Post reporting.

This government involvement reflects an economic positioning beyond traditional technology policy. The US federal government's policy environment incentivizes AI and associated energy infrastructure investment, with investment initiatives aligned with national security and economic growth objectives.

The policy framework encompasses multiple dimensions of AI development:

The regulatory environment has evolved to support rather than constrain investment, representing a significant shift from earlier technology policy approaches. The US enacted 59 new federal AI regulations in 2024, reflecting proactive governmental involvement in shaping AI development frameworks. However, unlike previous regulatory approaches that often stifled innovation through restrictive compliance requirements, current AI regulations focus on enabling responsible development while maintaining competitive advantages.

International competition has intensified government involvement globally, creating a complex geopolitical landscape for AI investment. Government investments span worldwide, including:

Each nation recognizes AI as critical infrastructure for maintaining economic competitiveness, but the approaches vary based on domestic capabilities and strategic objectives.

The global competition has created both opportunities and risks for private sector investors. Companies that align with government priorities can access substantial subsidies, tax incentives, and procurement opportunities. However, geopolitical tensions also create risks around international partnerships, supply chain dependencies, and market access.

The most successful AI investment strategies account for both the opportunities and constraints created by government involvement across multiple jurisdictions.

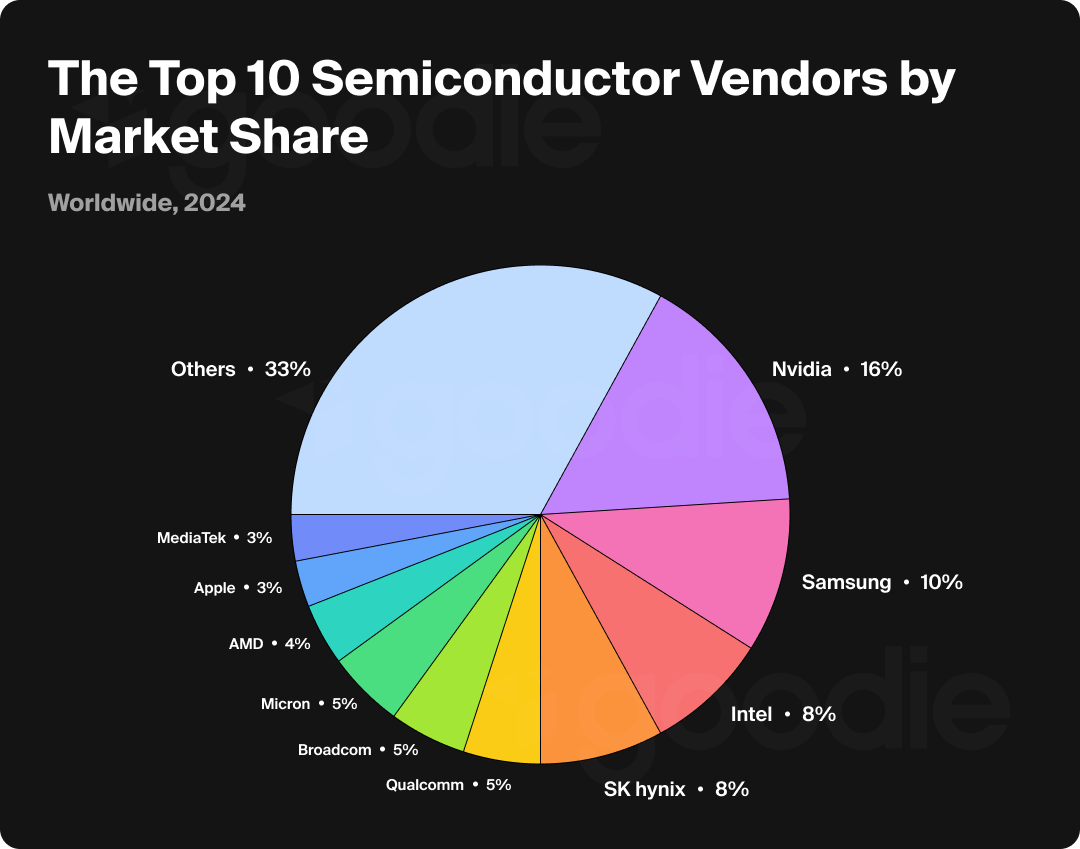

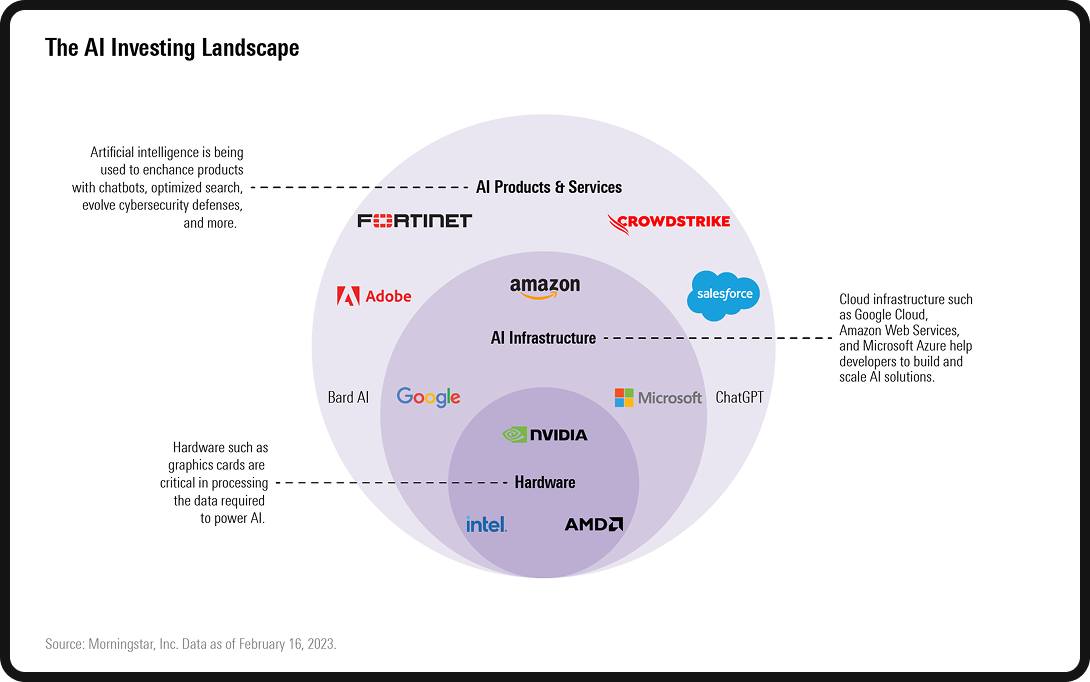

The semiconductor sector provides the clearest view of AI investment returns and competitive positioning by offering concrete evidence of how AI investments translate into measurable business results. Nvidia's revenue for 2024 is expected to surpass $61 billion (up from $4 billion in 2014) demonstrating the explosive growth potential in AI hardware. This revenue increase over a decade reflects market growth and Nvidia's strategic positioning at the center of the AI infrastructure buildout.

Market performance reflects this revenue growth with dramatic stock market valuations that have created enormous wealth for investors and employees. Nvidia dominates the AI chip market with stock price rises over 120% year over year and Q3 revenues up 94% year over year, driven by data center demand.

However, competitors are investing to challenge this dominance and creating opportunities for diversified investment strategies.

The competitive response has been significant across multiple dimensions of the semiconductor value chain:

These results indicate that the semiconductor investment opportunity extends beyond a single market leader to encompass the entire ecosystem of AI hardware.

The semiconductor investment opportunity has also driven innovation in chip architecture and manufacturing processes. Traditional CPU designs optimized for general computing prove inefficient for AI workloads, which require massive parallel processing capabilities. Graphics Processing Units (GPUs) filled this gap, but purpose-built AI chips offer even greater efficiency and performance. This architectural evolution has created opportunities for companies that can design and manufacture specialized AI semiconductors.

Strategic differentiation has emerged through custom silicon development that allows major technology companies to reduce dependence on external chip suppliers. Custom silicon chips designed by hyperscalers (like Google's TPU) enable optimized AI processing efficiency, according to Morgan Stanley's analysis.

This trend suggests that future AI leaders will control both software and hardware development and create vertical integration advantages similar to Apple's approach with mobile processors.

The custom silicon trend has significant implications for the broader semiconductor industry. While it creates competition for traditional chip manufacturers, it also increases demand for semiconductor manufacturing capacity and advanced packaging technologies. Companies that provide foundry services, electronic design automation tools, and specialized manufacturing equipment benefit from the increased complexity and volume of custom AI chip development.

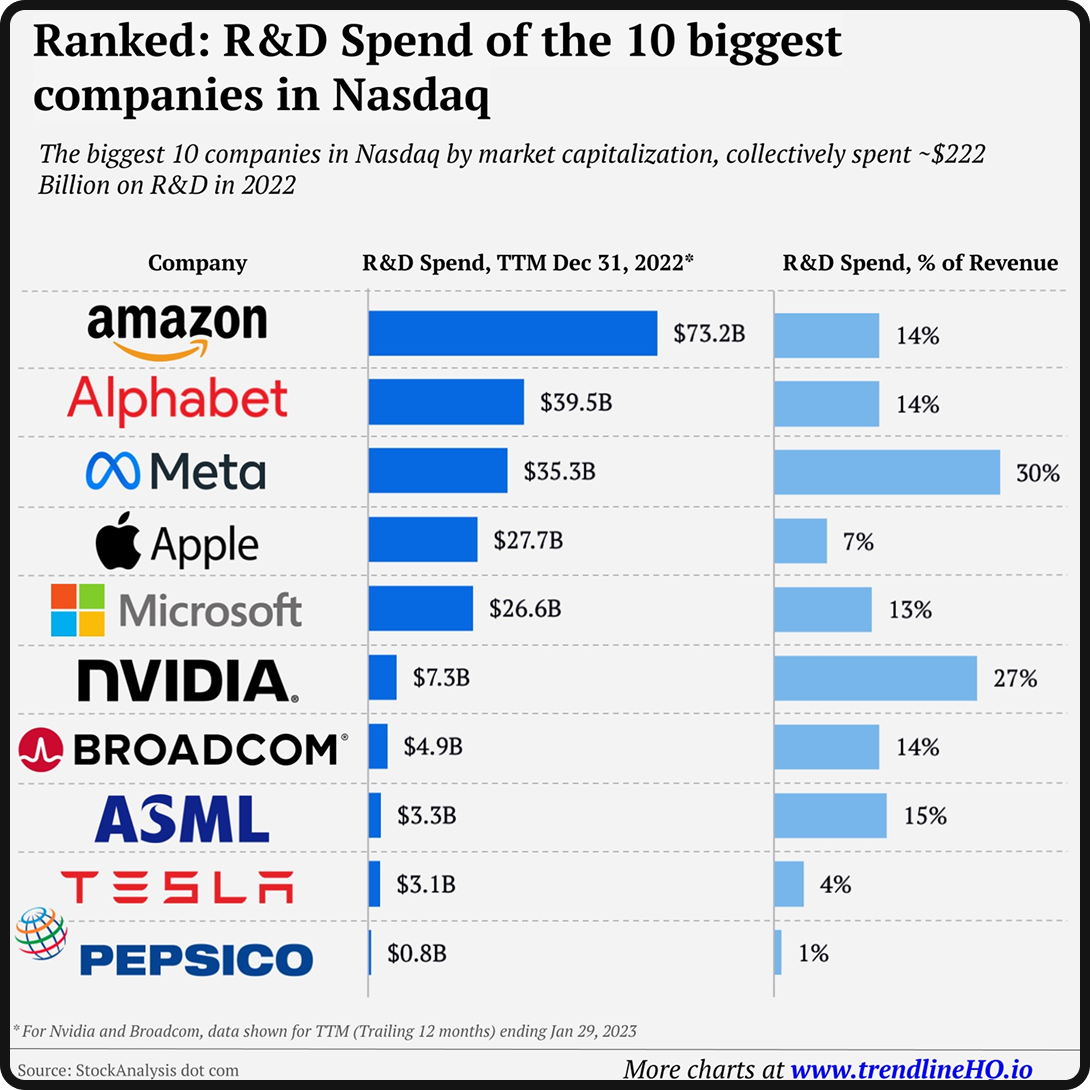

The AI investment surge has created an unprecedented concentration of research and development resources among a small number of technology giants, altering the innovation landscape. The Top 10 S&P 500 companies now account for over 40% of total research and development spending but only 13% of total revenue, signaling innovation concentration among technology giants.

This concentration reflects strategic rather than speculative investment patterns. AI investments favor chipmakers and cloud data center operators due to foundational infrastructure demand. However, the concentration also creates risks around innovation diversity and competitive dynamics. When a small number of companies control the majority of AI research resources, the direction of technological development becomes dependent on the strategic decisions of these firms.

The R&D concentration has accelerated talent acquisition competition to unprecedented levels. Leading AI researchers command compensation packages exceeding $1 million annually, with some AI researchers receiving equity packages worth tens of millions of dollars. This talent concentration creates positive feedback loops where the companies with the largest research budgets can attract the best talent, which enables them to develop superior AI capabilities, which generate the revenue to support even larger research investments.

Enterprise market adoption has validated these investment decisions across multiple industries and use cases. Palantir's US commercial segment grew 54% year over year in Q3 2024, reflecting expanding business AI adoption across industries and validating the enterprise market opportunity. However, the enterprise adoption pattern also reveals the challenges facing smaller AI companies competing against tech giants.

The innovation concentration has implications for startup companies and venture capital investment strategies. While early-stage AI companies can still achieve success by focusing on specific applications or vertical markets, competing with major technology companies on foundational AI capabilities requires access to resources that exceed the capacity of traditional venture funding. This dynamic has led to new investment structures, including partnerships between startups and major technology companies that provide access to computing resources and data in exchange for equity or licensing arrangements.

The most important and counterintuitive development in AI investment has been the dramatic improvement in economic efficiency with massive increases in total spending. The cost of running GPT 3.5 level inference models fell from November 2022 to October 2024, according to Stanford's AI Index. Simultaneously, the energy efficiency of AI deployments improved by almost 40% per year.

This efficiency improvement creates complex strategic dynamics that challenge traditional investment logic. Lower costs expand market accessibility, enabling more companies to adopt AI capabilities and creating broader market opportunities. However, efficiency improvements also compress profit margins and reduce the sustainability of competitive advantages based on AI access.

Companies must innovate to maintain differentiation as AI capabilities become commoditized.

The efficiency paradox has profound implications for competitive strategy. Early AI adopters could achieve advantages by having access to AI capabilities that competitors lacked. As AI becomes more accessible and affordable, competitive advantages must come from superior implementation, better data quality, more sophisticated applications, or integration with other business capabilities. This evolution favors companies with strong operational capabilities rather than those that have access to AI technology.

The efficiency trend has influenced infrastructure investment patterns in ways that seem contradictory but reflect underlying market dynamics. Cloud infrastructure migration accelerates as organizations seek scalable AI compute without heavy capital expenditures. This shift toward cloud AI solutions has benefited infrastructure providers while reducing barriers for smaller companies.

However, the most sophisticated AI applications still require substantial infrastructure investments. While basic AI capabilities become cheaper and more accessible, AI development requires enormous computational resources that exceed the capacity of standard cloud services. This creates a bifurcated market where routine AI applications become commoditized while advanced AI capabilities require significant capital investment.

The AI investment surge has created sophisticated opportunities for portfolio exposure that extend far beyond direct investment in technology companies. AI ETFs provide diversified exposure across segments like robotics, cloud software, and semiconductor firms, allowing institutional and retail investors to participate in AI growth without single company concentration risk.

The investment vehicle evolution reflects the maturation of AI as an investment theme. Early AI investments required identifying specific companies with promising technologies before their commercial potential became clear. Current investment opportunities span multiple asset classes, geographic regions, and stages of company development. Investors can choose exposure to AI infrastructure, AI applications, AI services, or companies that benefit from AI adoption without developing AI capabilities themselves.

The venture capital and private equity landscape has evolved toward investments that target specific business problems rather than broad technological capabilities. Private equity and venture capital pivot towards AI SaaS, recommendation engines, and customer-facing apps rather than foundational hardware.

This evolution reflects lessons learned from earlier technology investment cycles. The most successful technology investments often involve companies that apply existing technologies to solve specific business problems rather than companies that develop the underlying technologies. While foundational AI research requires capital investments with uncertain returns, AI applications can generate revenue and scale.

Market dynamics have shifted toward fundamental value creation as investor expectations mature beyond speculative growth. Valuation multiples are decreasing from unsustainable highs and there’s an emphasis on products demonstrating high ARR and profitability. This evolution suggests that AI investment is maturing beyond speculative positioning toward sustainable business model validation, creating opportunities for investors who focus on companies with proven revenue generation and clear paths to profitability.

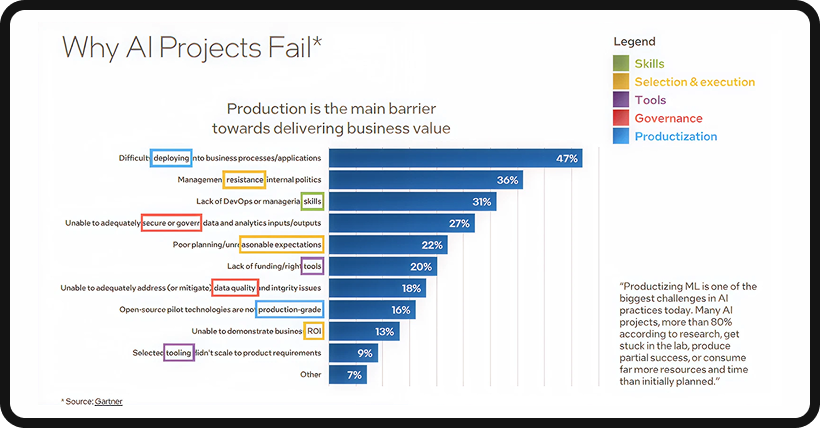

Strategic AI investment requires understanding operational failure modes that extend beyond technological challenges to encompass organizational, regulatory, and market risks. Up to 30% of generative AI enterprise projects risk failure due to inadequate data quality and weak operational controls, according to World Economic Forum research.

The failure analysis reveals critical success factors that often receive insufficient attention in investment evaluations. AI project failures often trace back to data quality and governance weaknesses rather than technology alone. This reality means that successful AI investment requires operational excellence frameworks and is a technological advancement. Companies with superior data management, change management, and organizational capabilities often achieve better results from AI investments than companies with superior AI technology but weaker operational foundations.

The operational challenges encompass multiple dimensions of business execution. AI systems require training data, but many companies lack the data collection, cleaning, and management processes necessary to support AI deployment. AI applications often require changes to business processes and employee workflows, but many organizations underestimate the change management requirements. AI systems need ongoing monitoring and maintenance, but many companies lack the technical capabilities to manage AI systems in production environments.

Environmental sustainability presents strategic risks that could constrain the growth trajectories of AI companies and limit investment returns. Energy consumption for AI workloads rises alongside efficiency gains, requiring balancing policies. Investors must evaluate whether AI companies can scale or if environmental constraints will limit growth trajectories as regulatory pressure increases around corporate environmental responsibility.

The environmental challenge creates both risks and opportunities for AI investment. Companies that develop more energy-efficient AI technologies or integrate renewable energy into their operations may achieve competitive advantages as environmental regulations tighten. Conversely, companies that rely on energy-intensive AI deployments may face increasing costs and regulatory constraints that limit their growth potential.

The evolution of AI capabilities will drive the next wave of investment opportunities as the technology progresses from current applications toward more sophisticated and autonomous systems. AI reasoning models approximate human logic, improving task complexity handling, suggesting that AI capabilities will continue expanding into higher-value applications that require complex decision-making and problem-solving capabilities.

The transition toward autonomous systems represents a fundamental shift in value creation that could dwarf the current AI investment wave. Autonomous AI systems that manage tasks within boundaries represent a significant evolution toward automation. This development could create new investment categories as AI evolves from a tool that augments human capabilities to an autonomous agent that can operate within defined parameters.

The autonomous AI trend has implications across multiple industries and applications:

Each of these applications represents substantial investment opportunities for companies that can develop reliable autonomous AI capabilities.

Enterprise focus on measurable returns will drive investment allocation toward AI applications that demonstrate clear business impact rather than technological sophistication. Enterprises focus on measuring AI return on investment with tools for performance and security, seeking measurable productivity gains. Companies will prioritize AI investments that demonstrate quantifiable business impact through cost reduction, revenue generation, or operational efficiency improvements.

This focus on measurable returns creates opportunities for AI companies that can provide clear value propositions and demonstrate return on investment. Companies that develop AI solutions for specific business problems with quantifiable benefits will attract more investment than companies that develop general-purpose AI capabilities without clear commercial applications. The investment landscape will favor companies that can articulate how their AI capabilities translate into improved business performance.

The $1 trillion AI investment wave represents a fundamental shift in technology value creation and competitive positioning that requires sophisticated strategic responses from business leaders and investors. Success requires understanding that AI investment extends beyond software and hardware to encompass energy infrastructure, regulatory compliance, operational excellence, and organizational transformation.

For business leaders, the strategic imperative involves building AI capabilities while maintaining operational discipline and financial prudence. The falling costs of AI deployment make capabilities more accessible, but they also make competitive advantages harder to sustain through AI access alone. Success requires strategic investment in AI capabilities combined with operational excellence in implementation, superior data management, and effective change management processes.

The most successful business AI strategies focus on specific applications with measurable business impact rather than broad AI initiatives with unclear value propositions. Companies should identify areas where AI can solve existing business problems, improve operational efficiency, or create new revenue opportunities. The investment should include AI technology and the operational capabilities necessary to deploy and maintain AI systems effectively.

For investors, the opportunity lies in identifying companies that can maintain competitive advantages in an accessible AI landscape. The companies that thrive will be those that solve the full spectrum of AI challenges, including infrastructure, energy, regulation, and operational execution. Investment strategies should favor companies with clear value propositions, proven business models, and superior execution capabilities rather than companies with impressive AI technology but unclear commercial applications.

The geographic concentration of AI investment in the United States and China creates both opportunities and risks that investors must navigate carefully. While these markets lead in innovation and funding, they also face regulatory scrutiny and geopolitical tensions that could disrupt investment flows. Diversified investment strategies that include exposure to AI development in other regions may provide better risk-adjusted returns than strategies concentrated in the dominant markets.

The convergence of AI with energy infrastructure represents the most significant long-term trend that will determine which companies and investors achieve superior returns. Companies that solve the energy equation for AI computing will emerge ahead in this investment cycle. This includes renewable energy generation and energy storage, grid management, and energy-efficient computing technologies.

The AI investment surge extends far beyond technology companies deploying capital for new hardware and software development. It encompasses a complete restructuring of how businesses operate, how governments regulate, and how investors evaluate opportunity. The winners will be those who understand that AI success requires solving challenges that extend far beyond algorithms and computing power into fundamental business strategy, operational excellence, and long-term value creation. The investment wave we're witnessing today will determine the competitive landscape for decades to come, making strategic positioning and execution more critical than ever before.

.svg)

.svg)

.svg)

.svg)